Pakistan closed December 2025 with a remittance inflow of $3.6 billion, a 16.5% year-on-year jump and 13% higher than November. The numbers, released by the State Bank of Pakistan, pushed FY26 (Jul–Dec) remittances to $19.7 billion, up 10.6%.

The surge helped cushion the external account, steady the rupee, and rebuild reserves. But beneath the headline success sits a structural question Pakistan can no longer dodge: are remittances buying time—or buying complacency?

The December spike, decoded

-

Total (Dec 2025): $3.6 bn (+16.5% YoY)

-

H1 FY26: $19.7 bn (+10.6%)

-

Top corridors: Saudi Arabia ($813 m), United Arab Emirates, United Kingdom, EU states, United States

-

External balance impact: Helped offset a $2.1 bn trade deficit in December; turned the current account to a $100 m surplus in November after October’s deficit.

Primary source (SBP):

Workers’ remittances, December 2025 — $3.6 bn (+16.5% YoY)

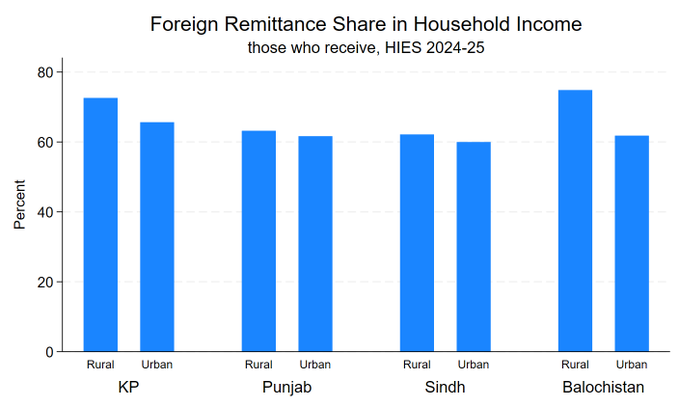

A quiet but crucial shift: who depends on remittances

HIES comparisons (2018–19 vs 2024–25) reveal a pivotal insight:

-

The share of remittances in recipient households’ income has stayed broadly flat.

-

But the fraction of households receiving remittances has increased sharply—especially in KP and Punjab.

Meaning: Pakistan’s remittance growth is not just the same families getting richer inflows; many more households now rely on foreign income. This expands social stability—but also widens macro-dependence.

Why Saudi Arabia matters more than ever

Saudi Arabia led December inflows and is central to the next phase. New defence–economic cooperation and 500+ pledged jobs point to sustained corridor strength. Short-term, that’s supportive for reserves and FX liquidity. Medium-term, it reinforces a model where labour exports substitute for goods exports.